PNN

New Delhi [India], May 22: Choosing between ULIPs and other investment options is not just about returns. It is about how you want to balance protection, growth, flexibility, and control. Many investors compare ULIPs with mutual funds, fixed deposits, or term insurance, but the comparison is not always straightforward.

A ULIP sits in the middle. It is neither a pure investment nor pure insurance. Understanding where it fits in your overall financial plan is more useful than trying to label it as better or worse.

What Is a ULIP and How Does It Work?

A Unit Linked Insurance Plan (ULIP) is a product that combines life insurance with market-linked investment. When you pay a premium, one part goes towards life cover, while the remaining amount is invested in funds such as equity, debt, or a mix of both.

ULIPs come with a mandatory lock-in period of five years, which means you cannot access your money during this phase. After that, partial withdrawals are allowed under certain conditions.

They also offer flexibility through fund switching, allowing you to move your investment between equity and debt depending on market conditions or your goals.

At the same time, ULIPs include multiple charges. These typically include premium allocation charges, fund management fees, mortality charges, and administrative costs. These charges are higher in the initial years and can affect early returns. This is why understanding the cost structure is important before investing.

Understanding Other Investment Options in India

Most traditional financial products in India are designed for a single purpose. You typically combine them to build a complete financial plan.

For example, mutual funds are focused on wealth creation. Fixed deposits are used for stability and capital protection. PPF is a long-term, tax-efficient savings option backed by the government. Term insurance provides life cover without any investment component.

Because of this separation, investors often hold multiple products at the same time. This gives more control, but it also requires more active management.

Each option differs in terms of liquidity, risk and tax treatment. Some allow easy withdrawal, while others enforce long holding periods. Some are market-linked, while others offer fixed returns.

Where ULIPs Differ from Pure Investment Products

The key difference between ULIPs and other options lies in structure. ULIPs combine two needs into one product. Most other options keep them separate.

This affects how they behave in real situations.

- ULIPs offer life cover along with investment

- Mutual funds offer only investment returns

- Term insurance offers only protection

ULIPs also come with a lock-in, which acts as a discipline mechanism. While this reduces flexibility, it can help investors stay invested during market ups and downs.

On the tax side, ULIPs allow deductions under Section 80C. Maturity proceeds may also be tax-free under Section 10(10D), subject to conditions. This creates a different after-tax outcome compared to many other products.

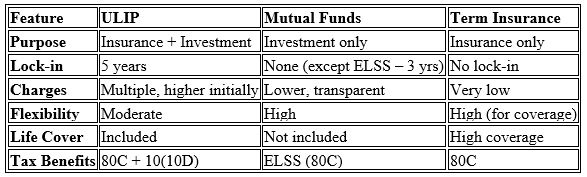

ULIP vs Mutual Funds vs Term Insurance: A Practical Comparison

Here is a simple way to understand how these options compare:

This table highlights a key point. ULIPs are designed for balance. Other products are designed for optimisation.

The Insurance Angle: ULIP vs Term + Investment Strategy

This is where most decisions become practical. With ULIPs, you are combining insurance and investment into a single product. This makes things easier to manage. You pay one premium and track one policy. However, the life cover in ULIPs is usually linked to the premium and may not always be sufficient for your family's needs.

With a term insurance + mutual fund approach, you separate the two:

- Buy a term plan for high life cover at a low cost

- Invest the remaining amount in mutual funds

This gives more flexibility and often better cost efficiency. But it also requires discipline and active management.

There is no universal answer here. It depends on whether you value simplicity or control.

Who Should Consider ULIPs?

ULIPs are not meant for everyone. They work best for a specific type of investor.

They may make sense if you prefer a structured and bundled approach. If you do not want to manage multiple products, a ULIP simplifies things. It also helps those who struggle with investment discipline, as the lock-in prevents early withdrawals.

They can also fit well for people looking to optimise tax benefits while staying invested for the long term.

On the other hand, if you are someone who actively tracks investments, compares costs and prefers flexibility, you may find better alignment with separate products like mutual funds and term insurance.

Key Things to Check Before You Decide

Before choosing any option, step back and look at your situation clearly.

1. Start with your goal. If your priority is protection, a term plan is more efficient. If your focus is wealth creation, mutual funds offer more flexibility. If you want both in a single structure, ULIPs can fit.

2. Then consider your time horizon. ULIPs require patience. They are not suitable for short-term needs.

3. Also, look at costs in detail. Do not just compare returns. Understand how charges impact your money over time.

4. Liquidity is another factor. If you may need access to funds, ULIPs may feel restrictive in the early years.

5. Finally, ensure your life cover is adequate. Do not rely only on the ULIP component if your protection needs are higher.

Conclusion: Where ULIPs Actually Fit

ULIPs are best understood as a middle-ground product. They are not built to maximise returns like mutual funds, nor are they the cheapest way to get life insurance. Instead, they are designed for investors who want a single, structured solution that combines protection with long-term investment.

If you value flexibility, lower costs, and greater control, separating insurance and investments often works better. If you prefer simplicity, discipline, and a bundled approach, ULIPs can play a role in your portfolio.

You can also use a ULIP calculator to estimate potential returns and understand how charges may impact your investment over time. Ultimately, the right choice depends on how you prioritise convenience, cost, and long-term financial clarity.

(ADVERTORIAL DISCLAIMER: The above press release has been provided by PNN. ANI will not be responsible in any way for the content of the same.)